Pupin Initiative Expert Team

Infrastructure, Influence, and Illusion: The Real Economics of Serbia–China Relations

How China’s infrastructure dominance in Serbia masks asymmetric economics and rising strategic vulnerabilities

In the first years after the Eurozone crisis, marked by economic uncertainty and stagnation, the Serbian government opened the door to the idea that Chinese capital could play a prominent role in restoring desperately needed growth in an economy burdened by high unemployment and weak productivity. Integrating the country into the Belt and Road Initiative appeared to offer a pragmatic strategy for diversifying investments and accelerating infrastructure development. Large projects in transport, energy, and industry were presented as evidence that Serbia could attract partners beyond its traditional economic sphere.

For nearly a decade, the narrative that China is Serbia’s key economic partner - the country that “builds Serbia” and supports its development more than the West ever did - circulated widely in economic and political commentary. The slogan is politically effective, but the substance is different. Serbia has financed the majority of these projects through public borrowing, while Chinese companies have primarily appeared as contractors with guaranteed profit and limited transparency. Unlike European investments, which integrate Serbia into production chains and export markets, Chinese involvement has largely focused on state-driven megaprojects where political symbolism often outweighs economic efficiency. The cost of that symbolism will ultimately be borne by taxpayers, not by Beijing.

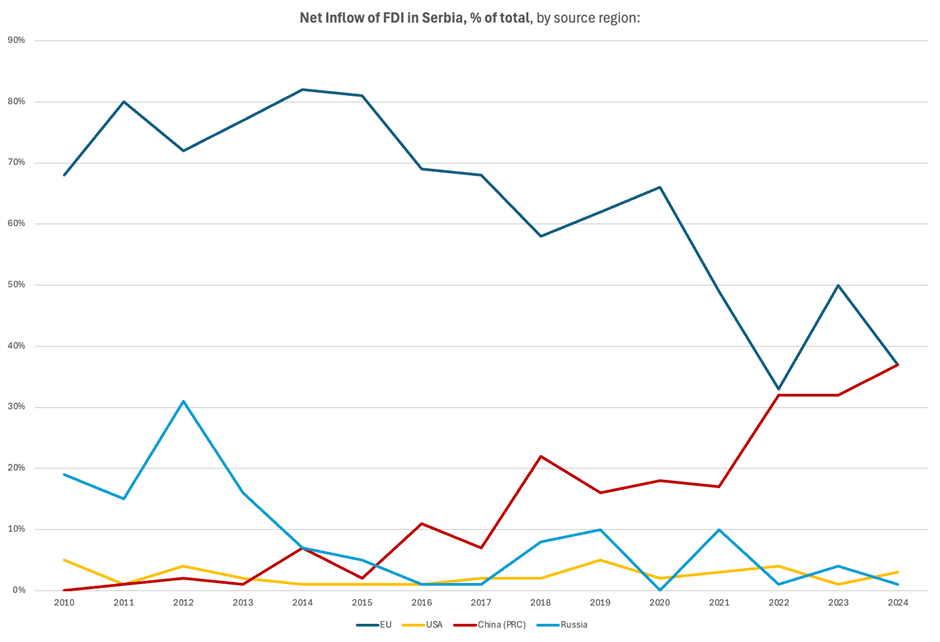

Source: National Bank of Serbia

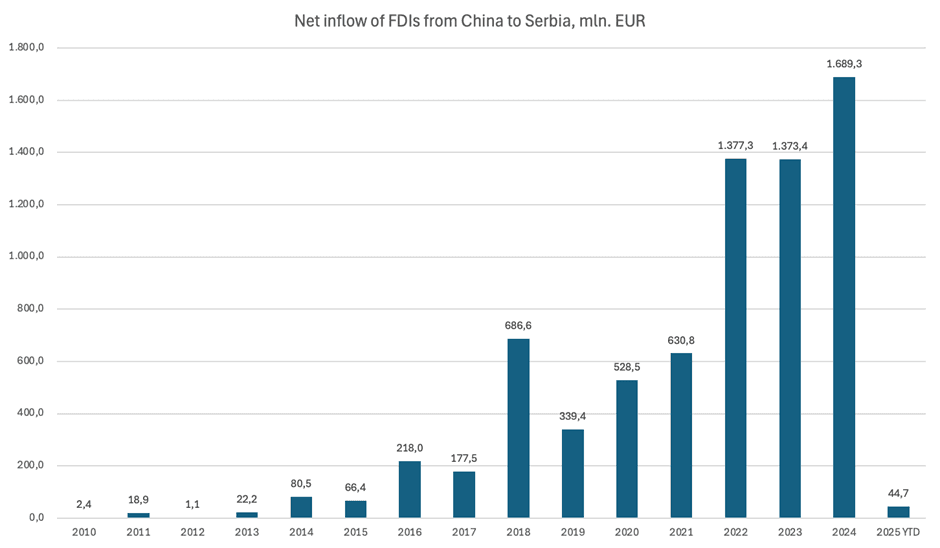

Over the past decade, China has become one of Serbia’s most visible economic partners. According to NBS data, from 2010 to 2023, China accounted for 14.3% of total FDI inflows into Serbia, making it the second-largest source of investment after the Netherlands (14.4%), which functions primarily as a holding location for multinational companies operating in Serbia. However, in the period between 2018 and 2023, China’s role expanded significantly: its share rose to 21.4%, placing it firmly in first position, with especially high annual shares recorded in 2022 (31.1%) and 2023 (30.4%). Total commitments are estimated at €4–5 billion in total, while €3.5 billion of this came not as market-based foreign investment, but as state-to-state loans tied to Chinese contractors, primarily through China Exim Bank. These loans financed a series of high-profile infrastructure projects, including the Belgrade - Budapest railway (Serbian section, €1.1 billion), the Pupin Bridge (€170 million), sections of the Belgrade ring road (over €300 million), and multiple highway segments across the country. In heavy industry, Chinese companies acquired major assets: HBIS purchased the Smederevo steel plant for a symbolic €46 million, later investing over €300 million into production, while Zijin took a controlling stake in the Bor copper and gold complex for €1.26 billion in 2018 and has since invested more than €2 billion in mine expansion. The Linglong tire plant in Zrenjanin, announced as a €900 million investment, became China’s most prominent manufacturing project in Serbia, though surrounded by regulatory and environmental controversy.

Taken together, China’s economic presence has been large in headline value and highly visible in concrete infrastructure, but structurally concentrated in sectors dominated by the state and dependent on public borrowing rather than in broad, market-driven investment that builds long-term competitiveness.

The rise of Chinese investment in heavy industry was accompanied by growing public concern over environmental conditions, particularly in Bor, Zrenjanin, and Smederevo. In Bor, Zijin’s expanded copper production significantly increased sulfur dioxide emissions, prompting repeated air-quality alerts and street protests in 2019, 2020, and 2021. In Smederevo, residents living near the HBIS steel mill reported persistent smog and dust, while in Zrenjanin, the construction of the Linglong tire plant triggered national attention over both pollution risks and labor conditions. These issues helped fuel some of the largest environmental demonstrations in Serbia in recent years: environmental protests in 2021 gathered tens of thousands of citizens across Belgrade, Novi Sad, and multiple smaller towns, signaling a broad shift from local grievances to nationwide public pressure for stronger environmental protection and regulatory oversight.

As said, the foundation of Serbia’s cooperation with China was established through intergovernmental agreements, rather than through open, competitive procurement. Major infrastructure projects were financed largely via state-backed loans from China Exim Bank, which included mandatory use of Chinese contractors and equipment. It also embodies confidentiality clauses that limit public access to cost structures and risk assessments - unlike in standard European or Western financing. These asymmetric features were present from the very beginning. However, the public became fully aware of their implications only with the emergence of Annex V, the classified pricing schedule for EXPO 2027 construction works. Annex V did not introduce new problems - rather, it made visible the structural asymmetry already embedded in the very model of intergovernmental cooperation itself. What also raises an eyebrow among financial experts is that Chinese loans generally exclude Paris Club comparability provisions, meaning that any potential future debt restructuring would be negotiated separately and likely under less favorable conditions for Serbia. The result is a system in which Serbia finances, while Chinese state-owned firms execute and profit, with limited transparency and increased long-term exposure for the public sector.

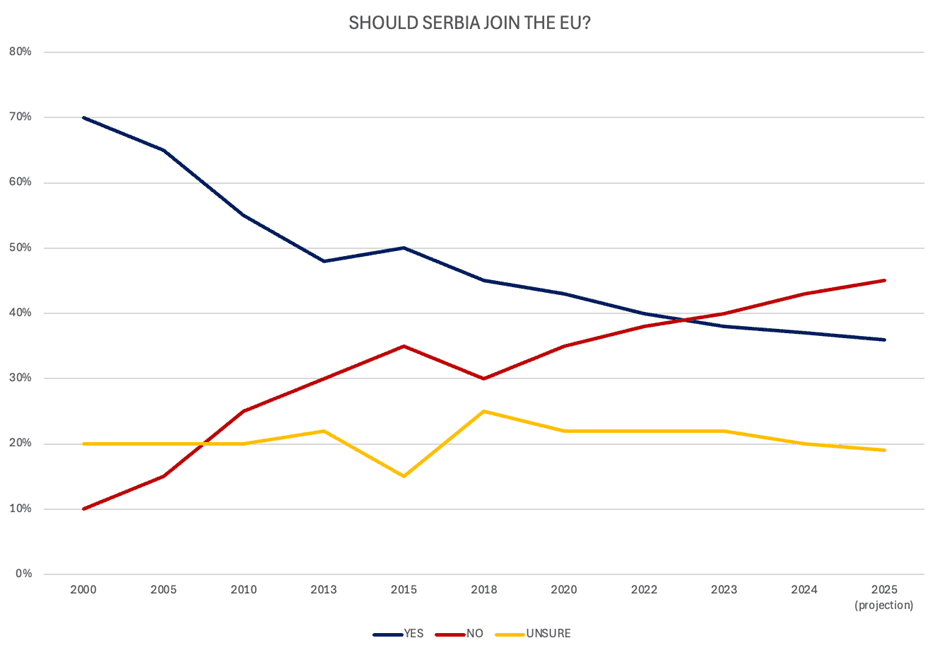

Source: Aggregated average of public opinion polling from multiple Serbian pollsters, compiled and standardized by the PI analytical team

The rise of Chinese investment in Serbia has coincided with a noticeable decline in public enthusiasm for EU membership. One may be quick to assume that this is a direct and deliberate outcome of Chinese foreign policy, but a more nuanced interpretation is necessary. The two trends are not directly causally linked. However, the growing visibility of Chinese-built infrastructure and revitalized industrial sites has played an important role in shaping public perceptions.

For many citizens, development is understood through what their eyes can see, and that is - a reopened steel plant in Smederevo, expanded mining operations in Bor, or newly constructed highways and railway corridors. Because these projects were frequently presented as symbols of partnership with Beijing, they contributed to the strengthening of anti-Western narratives that frame the EU as slow, conditional, and distant, and China as fast, tangible, and unconstrained.

This shift did not alter Serbia’s structural economic dependence on the European market, but it changed the emotional and political meaning of development, giving Chinese engagement a symbolic weight greater than its actual share in the economy.

Source: National Bank of Serbia

The political and economic “honeymoon” between Belgrade and Beijing has, in many respects, run its course. Annex V did not create tensions, but it revealed the limits of trust and transparency within the cooperation model itself. At the same time, China’s own regional priorities have shifted. After a decade marked by high-profile takeovers and state-financed infrastructure, Chinese investment momentum has slowed, with a significant decline in new Chinese capital inflows recorded in 2024 and the first half of 2025.

The model has reached saturation, and Beijing is now directing its strategic manufacturing investments primarily toward Hungary, where integration into the EU single market is more direct. What remains in Serbia are completed projects and long-term concessions - but without the same political enthusiasm or investment dynamism that characterized the previous decade.

Other Analysis

Read time:

7

min

Aug 6, 2026

text

How the Carpathian Initiative Could Redefine Serbia’s Role in Europe’s Future

The Carpathian Initiative could position Serbia as a key logistics hub for Europe’s future connectivity.

Read time:

15

min

Jul 28, 2026

text

Closing the Gap: Serbia and the Unfinished Map of the Three Seas

How completing the Initiative's Balkan core serves Belgrade, Brussels, and Washington alike, and why leaving it open invites others to fill it?

Read time:

12

min

Jul 22, 2026

text

Developing Serbia's Capital Market: How U.S. Financial Expertise and Investment Can Support Economic Modernization

How U.S. financial expertise and development finance can deepen Serbia’s capital market, curb reliance on opaque financing?